How to Save $1,000 in a Year or Less

Our readers always come first

The content on DollarSprout includes links to our advertising partners. When you read our content and click on one of our partners’ links, and then decide to complete an offer — whether it’s downloading an app, opening an account, or some other action — we may earn a commission from that advertiser, at no extra cost to you.

Our ultimate goal is to educate and inform, not lure you into signing up for certain offers. Compensation from our partners may impact what products we cover and where they appear on the site, but does not have any impact on the objectivity of our reviews or advice.

Life is full of unexpected expenses. No matter what life throws at you, having at least $1,000 in savings can help curb those financial surprises. Here are some simple, practical ways to save $1,000 in a year or less.

Our number one goal at DollarSprout is to help readers improve their financial lives, and we regularly partner with companies that share that same vision. If a purchase or signup is made through one of our Partners’ links, we may receive compensation for the referral. Learn more here.

Life is full of unexpected expenses.

You get a flat tire, have to take your child to the emergency room, or need to replace a broken washing machine.

No matter what life throws at you, having at least $1,000 in savings can help curb those financial surprises. Unfortunately, nearly a quarter of Americans have no savings at all.[1]

If this is you, take comfort that you’re not alone. But don’t wait until your next financial setback to make a chance. Now is the time to get ahead and create a basic emergency fund. Many financial experts recommend saving $1,000 to start.

Before You Save $1,000

Before working through the steps to save your first $1,000, laying a solid foundation will help keep you focused.

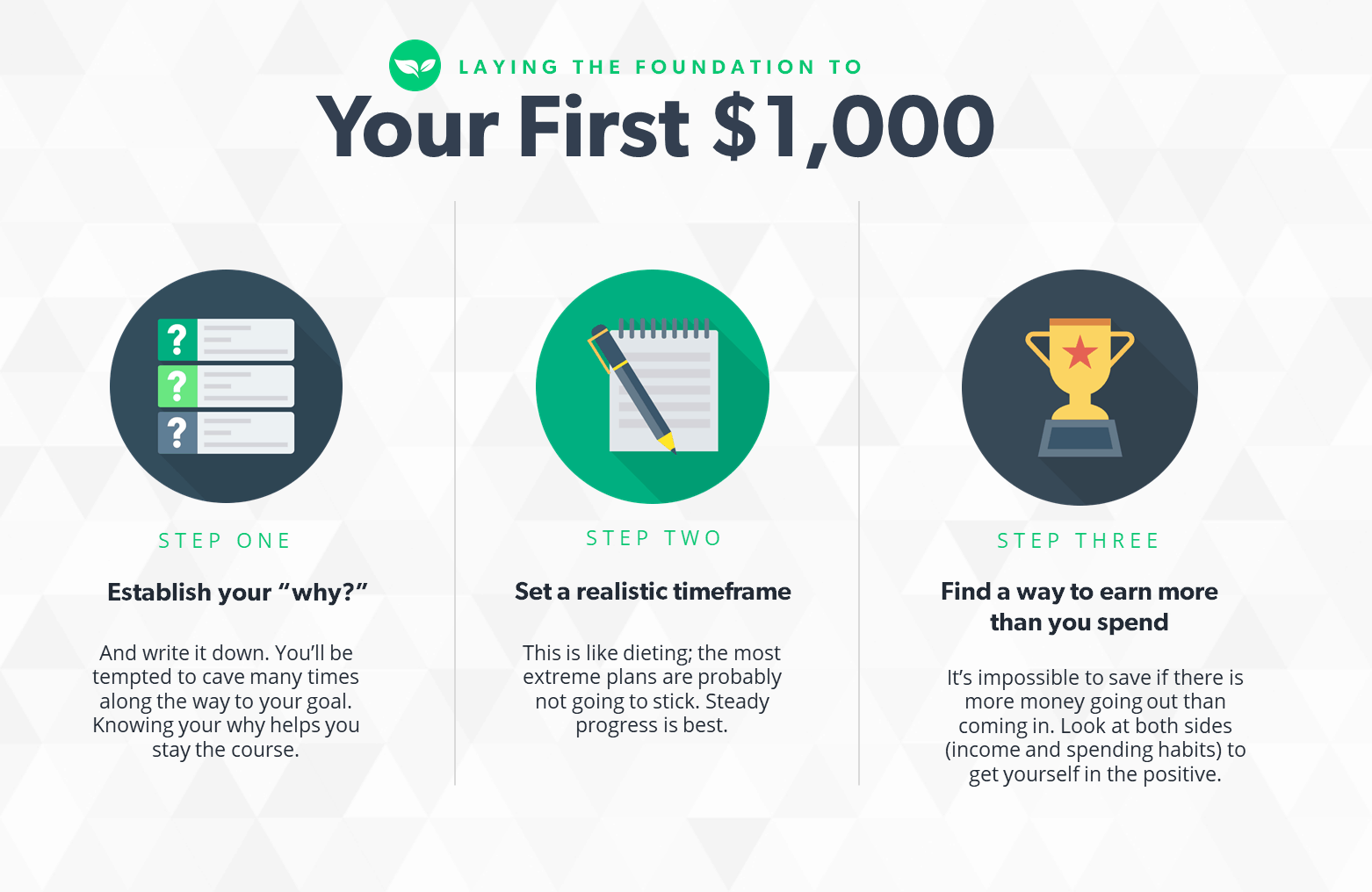

Establish Your “Why”

Before you start saving, think about why you want to save and what motivates you to reach your goals.

Are you living paycheck to paycheck? If so, a savings account will alleviate financial stress and prepare you for the unexpected. Do you have a family? Your savings will help you maintain financial stability for those you love, even when you’re faced with uncertainty.

Getting clear on your why helps you prioritize saving. Changing your spending habits to start an emergency fund might not seem appealing, but temporarily cutting your expenses to prevent taking on debt or to prepare for your children’s financial future may be more motivating.

Your motivation for saving money doesn’t have to be deeply meaningful or profound. Maybe you’re motivated by extrinsic rewards. If that’s the case, your why could be as simple as the spending splurge you’ve promised yourself once you reach your goal.

Whatever your reason is, get clear on it before you start saving. This is what will keep you going on the days it seems impossible to save $1,000.

Set an Attainable Savings Goal

Next, set an attainable savings goal. If you haven’t been successful at saving money in the past, it’s OK to start small. Set a goal like saving $100 in a month. If that seems too high, start with $50. Even $10 or $20 per month is a good place to begin.

The goal is to make saving money a habit. If you can achieve your goal, you’ll become more confident in your abilities, and you can build on your success.

As you succeed in saving money each month, increase your savings goal for the next month. If you’re saving $10, try upping it to $20. If you’re saving $75, increase to $100 or $150. Do what you can in a manner that’s comfortable for your budget and before you know it, you’ll be closer to your goal of saving $1,000.

Financial success is all about small but consistent steps over time. You don’t have to save $1,000 by next week. Just start with the first step.

Earn More Money Than You Spend

The savings formula is simple: income – expenses = savings. You can increase your savings in one of two ways: earn more, spend less, or both.

It sounds simple, but saving money only happens when you make more money than you spend. If you’re spending as much as you make, you won’t be able to accumulate savings because you won’t have any money left over. And if you spend more than you earn, you’ll end up in debt.

Increase the income portion of the equation by starting a side hustle to bring in some extra cash.

If you’re already working a full-time job and caring for family, you might not have time to earn more money. If that’s the case, focus on the expenses side of the equation. Take a look at your expenses and figure out if there’s anywhere you can cut.

7 Steps to Saving $1,000 for When You Need It

Use this step-by-step guide to create a plan and save your first $1,000.

1. Know Your Income and Expenses

Find a few minutes to sit down and add up how much you make each month. Include wages, tips, commissions, and any other income. Then use your previous months’ bank and credit card statements to calculate your current spending, including categories like eating out, groceries, gas, and other expenses that vary month to month.

Once you do this exercise, you’ll see exactly how much money is left over for savings. Then you can find ways to change the equation. Look for low-hanging fruit where you can reduce your spending without compromising your lifestyle.

For example, how much could you save by packing your food rather than going out to eat for lunch at work? If you have a tendency to buy clothes you see in Facebook ads but never end up wearing them, consider deleting the app from your phone or using an app like News Feed Eradicator to block your Facebook feed on your computer.

Creating a simple budget will help you see how much money is coming in and how much is going out each month. From there, you can determine how much to set aside for your $1,000 savings goal.

2. Set a Target Date to Reach $1,000

Once you decide how much you can save each month, choose a realistic date for your savings goal. If your goal is to save $100 a month, then it will take 10 months to reach $1,000.

Your savings goal should be a minimum amount you plan to save each month. Anything leftover at the end of the month can be put toward saving or split between your goals and extra spending.

Let’s say you set aside your planned $100 for savings. At the end of the month, you have $100 leftover that you planned to spend but didn’t. You can put the entire amount toward your goal or use some for savings and treat yourself with the rest. This can help you reach your savings goal faster and stay motivated along the way.

For added motivation, consider trying the 52-week money challenge. The goal of the challenge is to save $5,000 in one year. However, you can adjust the weekly savings amounts to fit your budget.

3. Determine the Amount to Save From Each Paycheck

A monthly savings goal is fine if you get paid once per month. But if you receive multiple paychecks per month, it might make more sense to set a savings goal for each paycheck.

After you determine an amount, talk to your payroll department or human resources. They can usually split your paycheck between two accounts so the money won’t even reach your main checking account. You can also set up automatic transfers from your checking to your savings.

This way you don’t have to rely on yourself to transfer the funds. Your savings is guaranteed.

4. Save Money in a Separate Account

Saving your money in a separate account is one of the most important steps in this process. When it’s out of sight, so is the temptation to spend it. An online savings account is a great option for most people. You’ll keep your savings separate from your checking account, and most online savings accounts offer higher interest rates than brick-and-mortar banks.

This is how I keep myself from dipping into my savings account. Our emergency fund is kept separate from the rest of our money, and it takes a few days to transfer funds to our checking account.

I have to think long and hard before transferring money from savings to checking. This gives me time to determine if something is truly an emergency and make a rational decision rather than an impulsive one.

5. Automate Your Savings with an App

Micro-saving apps can help you build a savings habit by setting aside a few dollars or cents at a time. Qapital is one of the most widely used of these apps.

Qapital users set rules for how to save money. With the round-up rule, Qapital rounds your transactions up to the nearest dollar and saves the difference. If you spend $45.01 at the grocery store, the app will round the transaction to $46 and transfer the extra $0.99 to a savings account.

Other Qapital savings rules allow you to save money when you get paid, work out, or indulge in a guilty pleasure.

6. Revisit Your “Why” When Tempted to Tap into Savings

We’ve all been there. You see something you want and get tempted to pull from your savings account to buy something.

Remembering your why will help you stay motivated in those situations. Your why will remind you that it’s important to leave your savings account alone.

Write down your reasons for saving money and display them somewhere you’ll see every day. If your motivation for saving is to buy the new pair of shoes you’ve promised yourself for reaching your savings goal, then hang a picture of the shoes on your refrigerator and put a reminder in your phone to keep it fresh in your memory.

7. Find One Big Expense to Cut

A painless way to save $1,000 quickly is to cut one big expense. Cancel your gym membership. Cut the cable. Skip dinners out. Any expense in your budget that isn’t necessary or doesn’t add value to your life is money you can put toward your savings.

These sacrifices can be temporary while you’re building your savings fund. Sometimes, it’s easier to make one or two decisions to cut something big than to make many small frugal decisions, like learning how to coupon or switching to generic brands.

Save $1,000 Faster by Making More Money

If there isn’t much room in your budget to cut spending, look for ways to increase your income.

Start with your current job. If it’s been a while since you negotiated your pay, then consider asking for a raise. The best way to approach this conversation is to gather information in advance about your performance and previous work. Once you have a solid case for why you’ve earned a pay increase, schedule a meeting with your manager to present your reasoning.

Another option is to pursue opportunities outside of your regular job. There are many side hustles you can do online with the skills and experience you already have. You can also apply for part-time or seasonal jobs in your area.

By increasing your income and focusing on the areas that have the biggest impact on your monthly budget, you can save $1,000 in less time than you may think. And that $1,000 can make all the difference the next time you’re faced with a financial emergency.